Everyday we are chasing for more and more money, in order to provide better life to yourself and especially to your loved ones. We always told ourselves that once we reach 1 Million example, we will quit job and spent your finite precious time with your love ones.

However, it’s never enough. When we have 1 million, we will aim for 2 millions. When we have 2 millions, we will aim for 3 millions, 5 millions, 10 millions, 100 millions….in the process you become old and tired….then suddenly you may realised that

“LATER may never come”…

Your kids grew up and they no longer need you to accompany them. They no longer want to sit on your lap to share/do things with you…all these time you spent in your 9 to 6 or even longer cubicles…can the money that you have earned by you buy back these?

We always thought we have more time with our old parents, but we are wrong. Time with them is ticking away every day. One day it will suddenly be gone. There is no regret medicine, no reset in time. Gone is gone and cannot come back. No matter you are billionaires or millionaires, you cannot reset this.

We always thought that we have more time with our spouse every day, but we are wrong. One day they will be gone too. When you read this, please go tell your spouse that you love him/her and he or she is the best thing that you ever had in your life.

Watch this:

These are the Lyrics

[ISABEL] When we first met Your heart was free Your hopeful eyes Saw only me

Now you’re looking for something Something I can never be When you are really All I need

You keep on telling me “later” But “later” never comes around Please stop telling me “later” As you search for what just can’t be found

Take my hand Come with me now and we’ll fly free No more “later”, we both know that’s a lie Don’t let be this the day I say

Goodbyе Goodbye

[SCROOGE] When you met hеr You were set free Her love for you Was plain to see

You kept looking for something A measure of security But she was really All you’d need

You kept on telling her “later” But “later” never comes around Please stop telling her “later” Stop searching for what can’t be found

Take her hand Go with her now and you’ll fly free No more “later”, we both know that’s a lie This will be the day she says Goodbye

Everyone wants to grow their wealth and get more and more money for the betterment of their life. But how to get more money? There is always a constant fight between the earn more and save more camp. If you know what I am talking about, are you in the earn more or save more camp? I am the earn more camp but if really can’t earn more, do your save more.

Earn More or Save more?

Should you Earn more or Save more?

Let’s say for a fresh grad with an employed income of 3k monthly, how much investing capital do you need to get $3000 monthly at 5% interest rate (I am assuming REIT ETF at 5%)?

Investment capital = Annual income / interest rate

Investment capital = $36,000 / 0.05

Investment capital = $720,000

Therefore, to generate $3000 monthly with a 5% interest rate (assuming a REIT ETF with a consistent 5% return), you would need approximately $720,000 in investing capital.

Is it easier to get $720,000 to generate $3000 monthly or is it easier to get $3000 monthly from your employed income?

If we up the amount further

Let’s us up the amount further. Let’s say if you have worked a few years and earn more now, at $5000 per month. How much investing capital do you need to get $5000 monthly at 5% interest rate (I am assuming REIT ETF at 5%)?

Investment capital = Annual income / interest rate

Investment capital = $60,000 / 0.05

Investment capital = $1,200,000

Therefore, to generate $5000 monthly with a 5% interest rate, you would need approximately $1,200,000 in investing capital.

1.2 Millions! Is it easy to get that 1.2 millions in the first place?

Let’s up the amount even further

Let’s us up the amount even further. Let’s say if you have worked a few years and earn more now, at $8000 per month. How much investing capital do you need to get $8000 monthly at 5% interest rate (I am assuming REIT ETF at 5%)?

Investment capital = Annual income / interest rate

Investment capital = $96,000 / 0.05

Investment capital = $1,920,000

Therefore, to generate $8000 monthly with a 5% interest rate (assuming a REIT ETF with a consistent 5% return), you would need approximately $1,920,000 in investing capital.

1.92 Millions! Is it easy to get that 1.92 millions in the first place?

Saving

Let’s talk about saving. If you earn 3k, and let’s say you are very thrifty and save up to 50% of your income, how long do you need to get $720,000?

Time = Desired savings amount / Monthly savings amount

Time = $720,000 / $1,500

Time ≈ 480 months = 40 years!

How many 40 years in life do you have?

Using the same example earlier and up the amount

Let’s talk about saving with increased income. If you earn 5k, and let’s say you are very thrifty and save up to 50% of your income, how long do you need to get $1,200,000?

Time = Desired savings amount / Monthly savings amount

Time = $1,200,000 / $2,500

Time = 480 months = 40 years

Another 40 years! Can you live that long?

Let’s up more and use the previous example

Let’s talk about saving with increased income. If you earn 8k, and let’s say you are very thrifty and save up to 50% of your income, how long do you need to get $1,920,000?

Time = Desired savings amount / Monthly savings amount

Time = $1,920,000 / $4,000

Time = 480 months = 40 years

OMG! Another 40 years! Can you live that long?

But let’s say your saving rate is higher at 70%

If you earn 3k, and let’s say you are very thrifty and save up to 70% of your income, how long do you need to get $720,000?

Time = Desired savings amount / Monthly savings amount

Time = $720,000 / $2,100

Time ≈ 343 months = 28.6 years

If you earn 5k, and let’s say you are very thrifty and save up to 70% of your income, how long do you need to get $1,200,000?

Time = Desired savings amount / Monthly savings amount

Time = $1,200,000 / $3,500

Time ≈ 343 months = 28.6 years

If you earn 8k, and let’s say you are very thrifty and save up to 70% of your income, how long do you need to get $1,920,000?

Time = Desired savings amount / Monthly savings amount

Time = $1,920,000 / $5,600

Time ≈ 343 months = 28.6 years

Let’s summarise

What happen now? Let me put everything in a table.

Get the idea?

I guess you have got the idea.

Capital that you have is the gist of your investment. You must be able to get that investing capital in the first place. To get large amount of investment capital, the easiest way is the earn it, not save it! There is a limit of how much you can save given that one always need some decent amount to maintain a decent standard of living.

It’s easier to save 50% if you are earning 8k per month as compared to 3k per month. Earning 8k per month and save 50% means you are saving 4k per month. Earning 3k per month and save 50% means you are saving 1.5k per month. It’s easier to live with 4k per month as compared to 1.5k per month. All these are assuming there is no lifestyle inflation.

Lifestyle inflation

Lifestyle inflation is when people start spending more as they earn more money. You know, it’s like when you get a raise and suddenly feel the urge to upgrade your lifestyle by buying fancier stuff or treating yourself to expensive things.

Let me give you an example:

Imagine this guy named Tan Ah Gao. He used to earn $50,000 a year and saved 20% of his income, which was $10,000. He was pretty frugal and careful with his spending. But then, his income jumped to $80,000 per year. And you know what happened? John thought he could afford a better lifestyle, so he moved to a more expensive apartment, bought a new fancy car, and started splurging on lavish vacations and fine dining. The problem was, all this extra spending made it hard for him to save the same 20%. So instead of saving $16,000 a year, he ended up saving only $8,000. See, lifestyle inflation is something that hunt everyone.

But…think in terms of the Time of your Life

How to control lifestyle inflation? It’s all in your mind.

Let’s say you wanted to spend $1000 to buy latest phone but you can actually just buy $300 decent phone. Many thinks opportunity cost is $700 but it is not. Instead Think this way: you earn let’s say $10 an hour, you are using 70 hours of life, 4200 minutes of your life, 25200 seconds of your life to get this. Worth it? If you think this is worth, go ahead. If not, do reconsider your options.

(Of course, if selfishly, please buy the latest iphone gadgets please, or else how to keep increase APPL EPS and dividends =p?)

SO Save more or Earn more?

Both saving more and earning more play crucial roles in building wealth. To me, both are important, but Earn more is more important because there is a limit on how much you can save based on your current earnings! Of course, do take note of lifestyle inflation.

Unlock your Mental Strength to Grow Wealth!

For those who issue of saving, think of your time spent to earn that money before you spend on something. For those who already save the maximum until your lifestyle standard cannot be minimize anymore, focus to build your career/business and earn more!

Build your capital and ultimately one day let your investing income > expenses. Then you will be free!

Remember: Earning more and save more is the key to unlock your wealth growth!

Lastly, I want to end with this food for thoughts:

Many may not understand this – the way you invest your money when you have 10k capital as compared when you have 1 million capital is very different. I don’t understand it in the past, but I understood it now.

Good articles that you should read!

People are drawn to dividend investing.

Why? Firstly, dividends provide a regular stream of income, allowing investors to receive a portion of the company’s profits on a periodic basis. This can be particularly attractive for individuals seeking consistent cash flow or looking to supplement their existing income. Additionally, dividend investing is often viewed as a more stable and predictable investment strategy compared to relying solely on capital appreciation.

I always write and share articles, especially on dividends which many people love them. Do read them!

Alternatively, you can go the right side of my page, there is a search bar where you can simply search “dividend” to see all my articles related to dividends!

Of course, you can search for other things that would interest you such as “Careyourpresent”, “Reits”, “Side Hustles”, “Fixed Incomes”, “Savings” etc.

CAREYOURPRESENT

Money just buy you the chance of freedom.

When you are young and working, you exchange time for money. When you are old, you can have lots of money but you can’t buy time back, especially the things that you have missed while busying striking out in career. Of course, if you love your career, and consciously know that you are missing out the first time your child walk or talk, that’s ok, but if you are the other spectrum, please do something about it.

Your kids grew up and they no longer need you to accompany them. They no longer want to sit on your lap to share/do things with you…all these time you spent in your 9 to 6 or even longer cubicles…can the money that you have earned by you back these?

We always thought we have more time with our old parents, but we are wrong. Time with them is ticking away every day. One day it will suddenly be gone. There is no regret medicine, no reset in time. Gone is gone and cannot come back. No matter you are billionaires or millionaires, you cannot reset this.

We always thought that we have more time with our spouse every day, but we are wrong. One day they will be gone too. When you read this, please go tell your spouse that you love him/her and he or she is the best thing that you ever had in your life.

I have picked out some of the more life reflecting articles of the CAREYOURPRESENT series. Do read them:

You can read more about my articles on Careyourpresent via the Category “Careyourpresent” or simply click “Careyourpresent” via the main menu bar.

REMEMBER:

Love your life daily.

You have one less day with your spouse, parents, children and yourself.

Time is ticking away.

For each passing day,

Enjoy and Treasure your Life!

For those who are interested in regular updates of my articles, please join the others to sign up for my free newsletter to has my newest blogposts sent to your mailbox for free!

For real time exclusive updates on market news/life (especially Crypto markets where the news move fast, important news will be shared directly via tweets or telegrams), do also join the platforms below and engage with other like-minded people!

Telegram Group (Chat with me and other like minded people!)

If you’re looking referral codes, do check out my referral and ebook page. Give it a try and who knows? You might end up loving these platforms! To be absolutely fair to all the readers, I am definitely using all these companies and they are useful to me! Likely will be useful to you too!

At the same referral and ebook page, you can also download my free ebooks and other free resources.

For quick references to these resources, you can see below.

Ebooks and other useful resources on enhancing productivity (Investment, Excel, Notion etc). Currently most of it are free at this moment (subject to change).

WeBull: A powerful brokerage with nice free welcome gift. You can refer to my guide here on how to signup! 4 Simple step only! Click here to register a new account!

MoneyOwl: You can use this 6SHU-93MC to get free grab vouchers and highly safe liquid cash fund account.

Trust Bank – You will enjoy free FairPrice E-Voucher referral if you sign up via my referral code KNDBPEPT. Simply download the Trust Bank SG App on the App Store or Google Play Store. Tap on “Use referral code” immediately after you start the app and key in: KNDBPEPT

FSMOne: P0413007. Good account to keep liquid cash in autosweep and to purchase investment at low fee.

Hostinger: You can use this link for hosting your new website. 20% off hosting!

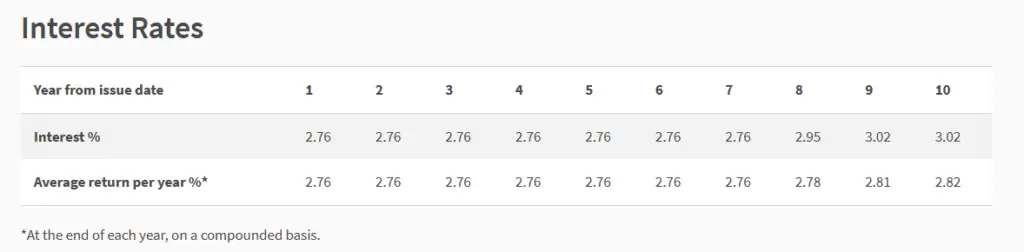

Many people love the stability of income, monthly cashflow, interests etc, worrying about the volatility of equities etc. Singapore Saving Bond is one of the best options that many people like to opt into. This month rate is out! The interest is no longer pretty but is still attractive. Why do I say so?

The rate for first year is 2.76% with 10-year rate at 3.02%. The average 10 years rate is 2.82%. Psychologically, below like to buy SSB with rate above 3%. However, this month and the previous month the rate starts to drop below 3%, hence people think that this is not attractive not pretty anymore. But if one think carefully, 3%-2.82% = 0.18%. Is that difference really that big?

The CAP of SSB is 200k per pax. Let’s say for 200k, 200k*0.18%= 360 per year, $30 per month. It’s not a lot but its decent for some cai png money. However, realistically, during the months where the rate is above 3%, it’s not easy to get all 200k inside. Hence, you won’t be able to get all your 200k to be above 3% within a month of application as you won’t know the allocation rate.

If you refer to the April bonds, actually you can get everything you want, it’s all about hindsight. But who knows before that? When it was 3% that time, but the other options at that time give up to 4%, people rather take other options. Now it’s 2.82%, people rather take other options or this option?

We should compare with other options available. One can see that the rates are dropping across board. The fixed deposits across the banks are around 3-3.5% for those 6 to 12 months. If you buy Fixed deposit, you will earn more as compared to Singapore Saving Bonds. But who know what will happen after 6 to 12 months? Singapore Saving Bonds, let you lock 10 years rate in advance and save you the hassle to keep sourcing for better rate every 6 or 12 months.

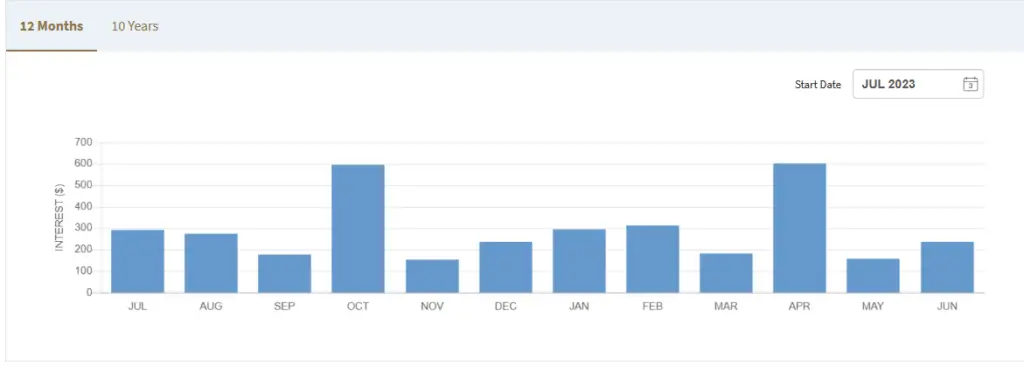

Is this hassle worth $30 per month for 200k worth of bonds? Or would you be better to spend your time better elsewhere? It’s up to individual. For me, I have finish building up my bond ladder where I will get something every month. Likely, I won’t add anymore. You can see screenshot of my bond ladder below.

Locked down decent rates of around 3% for 10 years.

Easy to redeem and can redeem partial

Liquidity needs maximum of 1 month where you can get your money back. Hence suitable as emergency fund.

Limit of 200k should be good enough for most people.

Can build Bond Ladder to get monthly income (which I already did)

Let’s us recap the disadvantages of SSB:

Short term rates are lower than banks’ fixed deposits, money market funds such as WeBull Fullerton fund etc of around 3.5% and above.

Low returns

1 month liquidity to redeem your funds may be too long for people who need the funds immediately.

Interesting SSB this month

Do note that if you want to apply, the deadline is 26 Jun 2023, 9pm, with allocation out on 27 Jun 2023, after 3pm. The amount offered is 600 millions.

In my humble opinion, this month should be interesting month for Singapore Saving Bonds. People think Fed may not increase rate in June and the fact that fixed deposit rate are dropping all across the banks which make fixed income hunter/savers worry if the rates will drop further. Some might want to get the chance to lock their money in care rate drop further in a 10-year flexible bonds where they can withdraw the money within 1 month notice. Hence, there may be some interest this month, but I don’t think will be overwhelming.

As for me, I have already created by Singapore Saving Bonds ladder as my emergency fund. I won’t add further. You can try creating bond ladders too. Getting few hundreds every month risk free is great! Instead, I have also been shopping for equities for the past few weeks. See below:

— Edmond | Careyourpresent (@careyourpresent) June 1, 2023

Good articles that you should read!

People are drawn to dividend investing.

Why? Firstly, dividends provide a regular stream of income, allowing investors to receive a portion of the company’s profits on a periodic basis. This can be particularly attractive for individuals seeking consistent cash flow or looking to supplement their existing income. Additionally, dividend investing is often viewed as a more stable and predictable investment strategy compared to relying solely on capital appreciation.

I always write and share articles, especially on dividends which many people love them. Do read them!

Alternatively, you can go the right side of my page, there is a search bar where you can simply search “dividend” to see all my articles related to dividends!

Of course, you can search for other things that would interest you such as “Careyourpresent”, “Reits”, “Side Hustles”, “Fixed Incomes”, “Savings” etc.

CAREYOURPRESENT

Money just buy you the chance of freedom.

When you are young and working, you exchange time for money. When you are old, you can have lots of money but you can’t buy time back, especially the things that you have missed while busying striking out in career. Of course, if you love your career, and consciously know that you are missing out the first time your child walk or talk, that’s ok, but if you are the other spectrum, please do something about it.

Your kids grew up and they no longer need you to accompany them. They no longer want to sit on your lap to share/do things with you…all these time you spent in your 9 to 6 or even longer cubicles…can the money that you have earned by you back these?

We always thought we have more time with our old parents, but we are wrong. Time with them is ticking away every day. One day it will suddenly be gone. There is no regret medicine, no reset in time. Gone is gone and cannot come back. No matter you are billionaires or millionaires, you cannot reset this.

We always thought that we have more time with our spouse every day, but we are wrong. One day they will be gone too. When you read this, please go tell your spouse that you love him/her and he or she is the best thing that you ever had in your life.

I have picked out some of the more life reflecting articles of the CAREYOURPRESENT series. Do read them:

You can read more about my articles on Careyourpresent via the Category “Careyourpresent” or simply click “Careyourpresent” via the main menu bar.

REMEMBER:

Love your life daily.

You have one less day with your spouse, parents, children and yourself.

Time is ticking away.

For each passing day,

Enjoy and Treasure your Life!

For those who are interested in regular updates of my articles, please join the others to sign up for my free newsletter to has my newest blogposts sent to your mailbox for free!

For real time exclusive updates on market news/life (especially Crypto markets where the news move fast, important news will be shared directly via tweets or telegrams), do also join the platforms below and engage with other like-minded people!

Telegram Group (Chat with me and other like minded people!)

If you’re looking referral codes, do check out my referral and ebook page. Give it a try and who knows? You might end up loving these platforms! To be absolutely fair to all the readers, I am definitely using all these companies and they are useful to me! Likely will be useful to you too!

At the same referral and ebook page, you can also download my free ebooks and other free resources.

For quick references to these resources, you can see below.

Ebooks and other useful resources on enhancing productivity (Investment, Excel, Notion etc). Currently most of it are free at this moment (subject to change).

WeBull: A powerful brokerage with nice free welcome gift. You can refer to my guide here on how to signup! 4 Simple step only! Click here to register a new account!

MoneyOwl: You can use this 6SHU-93MC to get free grab vouchers and highly safe liquid cash fund account.

Trust Bank – You will enjoy free FairPrice E-Voucher referral if you sign up via my referral code KNDBPEPT. Simply download the Trust Bank SG App on the App Store or Google Play Store. Tap on “Use referral code” immediately after you start the app and key in: KNDBPEPT

FSMOne: P0413007. Good account to keep liquid cash in autosweep and to purchase investment at low fee.

Hostinger: You can use this link for hosting your new website. 20% off hosting!