Risk Free Heaven Hunters

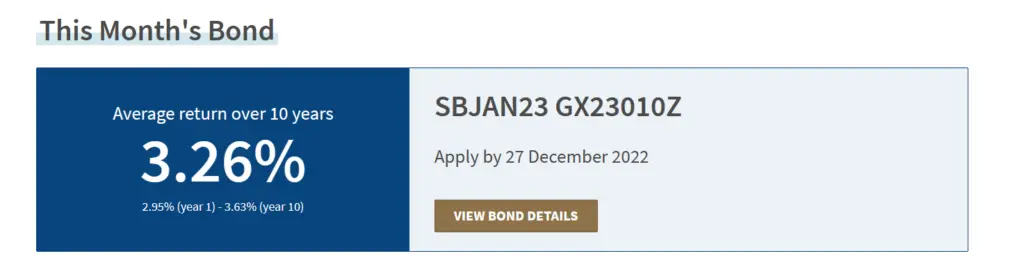

Currently we are in the best world condition where interest rates keep rising, I believe that many yields hungry, but more risk averse people are hunting for the best yield returns for their idling cash. Is the coming Singapore Savings Bonds SBJAN23 GX23010Z with average yield of 3.26% a safe and secure investment?

The recent MAS treasury bill is 4.28%, did you apply it? I did but didn’t manage to get. You can read from my past post below. Would I buy the upcoming SSB?

Upcoming Singapore Saving Bonds

SSBs are low-risk, long-term investment instruments issued by the Singapore Government. They offer a fixed rate of interest for 10 years and can be held for up to 10 years. They may be suitable for investors who are looking for a stable, low-risk investment with a long-term horizon. However, SSBs generally provide a lower short-term return as compared to other alternatives.

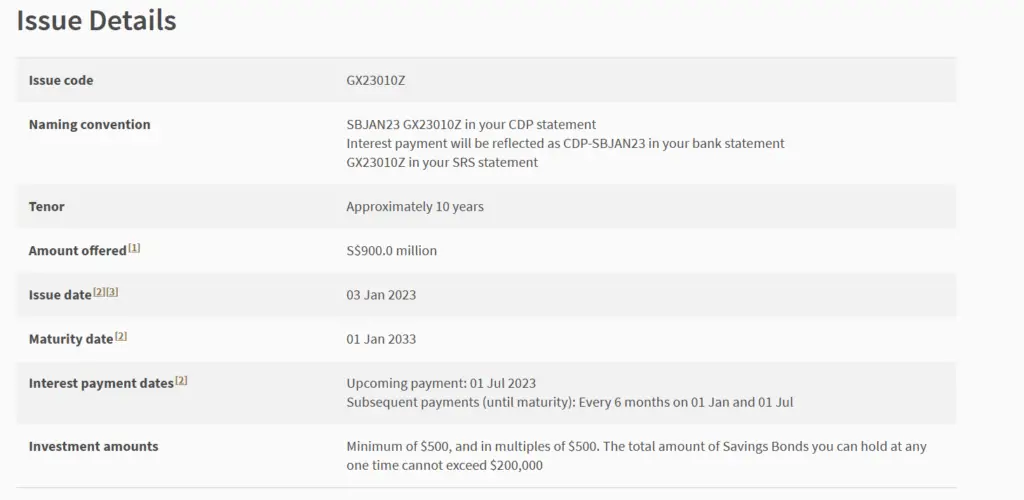

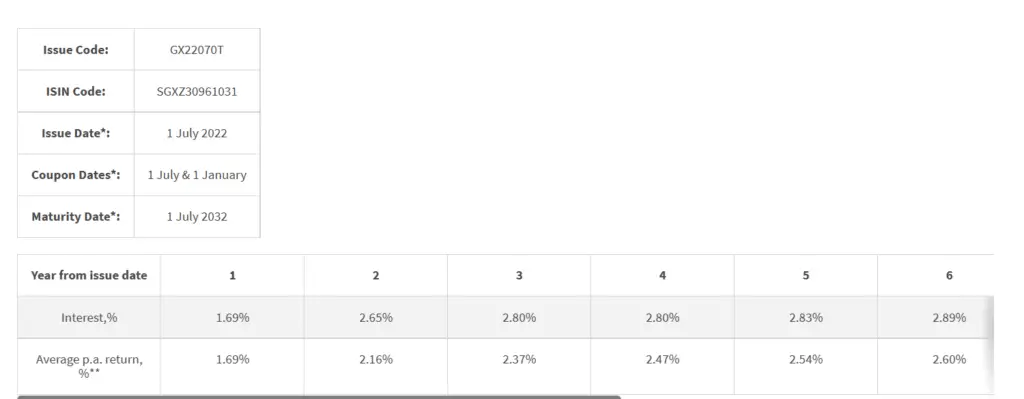

Let us look at the details of the upcoming bond – information for this issue below are extracted from MAS website.

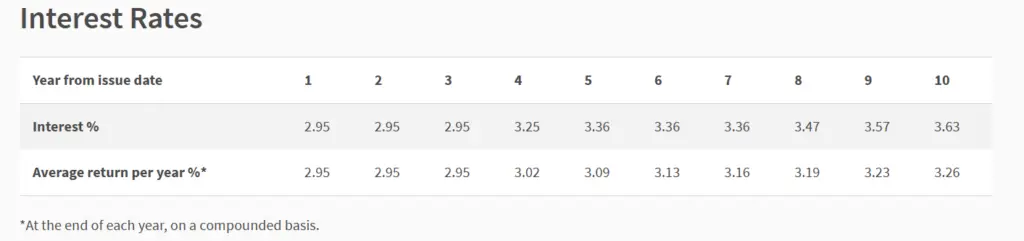

If we look at the tables above, you will get 2.95% on 01 Jan and 01 Jul half yearly for the first 3 years, after that it will increase to 3.25% followed by 3.36% until it reaches 3.63%. The average 10 years rate if you held for 10 years are 3.26%. Application deadline is tomorrow 9pm.

If we compared to other liquid cash option (Best places to put Liquid Cash now), this is very low.

Most people won’t not want to buy it on the first look. They can easily get more than 3% using local bank accounts or even Fixed Deposit. Why should I lock my money up for a miserable 2.95%? This doesn’t make sense.

Think Further

However please think further. Let us look at the 10 years treasury yields. The rates although drop as compared to few months ago but it is slowly rising back.

If we take a step back, the Federal Reserve, also known as the central bank of the United States, sets a target for the federal funds rate, which is the interest rate at which banks and other financial institutions lend and borrow money overnight. The Federal Reserve adjusts the federal funds rate in an effort to influence economic activity and maintain price stability.

Inflation is a measure of the rate at which the general level of prices for goods and services is rising, and subsequently, purchasing power is falling. Central banks, including the Federal Reserve, attempt to maintain price stability by setting an inflation target and using monetary policy to achieve it.

When the Federal Reserve raises the federal funds rate, it can signal to the market that it is trying to curb inflation.

Inflation rate is coming down but is still high. Although Fed is not pivoting but is slowly reducing rate hike, the 3-4% interest rate provided by the banks may maintain for a while but how long? By then if you want to come back to buy SSB, you may not have a chance to get an issue for more than 3%?

Other considerations

Let us also think of the advantages and disadvantages of SSB for this issue

- Decent long-term rate for above 3%

- Short term rate of 2.95% is decent compared to normal saving accounts

- High liquidity. Can redeem and take back the funds within a month (As I have mentioned previously, upcoming 2023 year the market will be back, keeping your funds liquid while earning some returns will give you the opportunity to earn generational wealth.)

- Backed by Singapore Government

Disadvantage of current SSB issue

- Lower returns as compared to other alternatives. While the rate may be higher than the rate offered by most savings accounts, it may not be as high as the potential returns offered by other types of saving alternatives

- Long-term investment horizon: SSBs have a maximum maturity of 10 years, which means that you will need to hold the bonds for a significant period of time in order to realize the full average return of 3.26%

What would I do?

As I have mentioned below, I am building SSB bond ladders for my emergency funds since July 2022 and have already completed it. I will be getting SSB return every month for the whole year of 2023, it’s a small amount but better than keeping it rot in normal bank saving accounts.

I will redeem the July 2022 issue as it only gives me 1.69% every July and January. Meanwhile, I will apply the current issue (which also pays every July and January) to replace my loss in SSB income for the months of July and January. Application deadline is 9pm tomorrow, please remember to apply by the deadline!

A picture speaks a thousand word. In case for those who are unsure what I mean by SSB bond ladder, let me end this article with my SSB bond ladder screenshot from the SSB portal. The Jan and Jul in the picture below will be gone after I redeemed my July 2022 issue tomorrow but will be replaced by the upcoming issue 🙂

Good articles that you should read!

People are drawn to dividend investing.

Why? Firstly, dividends provide a regular stream of income, allowing investors to receive a portion of the company’s profits on a periodic basis. This can be particularly attractive for individuals seeking consistent cash flow or looking to supplement their existing income. Additionally, dividend investing is often viewed as a more stable and predictable investment strategy compared to relying solely on capital appreciation.

I always write and share articles, especially on dividends which many people love them. Do read them!

- Simplified Guide to the Key Gist of Grant of Probate and Estate Planning

- Cheapest and best way to trade Singapore Stocks with CDP

- Mastering Dividend Investing: 5 Evergreen Investment Principles

- Unlock Lucrative Returns with IAPD: A High-Yield ETF Providing 7% Annual Yield and Quarterly Payouts

- Unlock Lucrative Returns with SDIV: A High-Yield ETF Providing 11% Annual Yield and Monthly Payouts

- If I am a dividend investor, this is what I would do….

- 7 Things to consider before buy a dividend stock

- 4 Dividend ETFs that can let you sleep well even in the scary bear market

- 5 Best Counters for Passive Dividend Investing

- The Three MOST Important Traits of an Investor

- What is the best investment strategy in the world?

- Ultimate Strategy of buying REITS: XXX instead of X000?

- Ultimate Free 2 Days Reit MasterClass: Exclusive at Careyourpresent.com only!

Alternatively, you can go the right side of my page, there is a search bar where you can simply search “dividend” to see all my articles related to dividends!

Of course, you can search for other things that would interest you such as “Careyourpresent”, “Reits”, “Side Hustles”, “Fixed Incomes”, “Savings” etc.

CAREYOURPRESENT

Money just buy you the chance of freedom.

When you are young and working, you exchange time for money. When you are old, you can have lots of money but you can’t buy time back, especially the things that you have missed while busying striking out in career. Of course, if you love your career, and consciously know that you are missing out the first time your child walk or talk, that’s ok, but if you are the other spectrum, please do something about it.

Your kids grew up and they no longer need you to accompany them. They no longer want to sit on your lap to share/do things with you…all these time you spent in your 9 to 6 or even longer cubicles…can the money that you have earned by you back these?

We always thought we have more time with our old parents, but we are wrong. Time with them is ticking away every day. One day it will suddenly be gone. There is no regret medicine, no reset in time. Gone is gone and cannot come back. No matter you are billionaires or millionaires, you cannot reset this.

We always thought that we have more time with our spouse every day, but we are wrong. One day they will be gone too. When you read this, please go tell your spouse that you love him/her and he or she is the best thing that you ever had in your life.

I have picked out some of the more life reflecting articles of the CAREYOURPRESENT series. Do read them:

- The Best Advice to Parents and Child

- What if Later never come?

- What will you bring with you on your last day on Earth?

- Time is the ultimate currency, not money

- Our Life only have 5 short Days – we should live the best for every day

- Truly understand Living in the Moment now

- 11 Important Unexpected Life and Money lessons to learn from Your Children

- The days are long but the years are short

- Ditch your mobile phone to build real life

- Careyourpresent: Time is the most important

- Careyourpresent: What is your purpose of life?

- Careyourpresent : Greatest Regrets in life

- Careyourpresent : You might not believe it. It’s little unexpected things that make up a real life

- Careyourpresent: Something only happen once in life, if you missed it, it’s gone forever…

- Careyourpresent : Why is Gold useful?

- Careyourpresent: Frozen. Let it go!

You can read more about my articles on Careyourpresent via the Category “Careyourpresent” or simply click “Careyourpresent” via the main menu bar.

REMEMBER:

Love your life daily.

You have one less day with your spouse, parents, children and yourself.

Time is ticking away.

For each passing day,

Enjoy and Treasure your Life!

For those who are interested in regular updates of my articles, please join the others to sign up for my free newsletter to has my newest blogposts sent to your mailbox for free!

For real time exclusive updates on market news/life (especially Crypto markets where the news move fast, important news will be shared directly via tweets or telegrams), do also join the platforms below and engage with other like-minded people!

- Telegram Group (Chat with me and other like minded people!)

- Telegram Channel (Get the latest updates on the markets/life!)

- RSS Feed

You may also contact me via [email protected].

If you’re looking referral codes, do check out my referral and ebook page. Give it a try and who knows? You might end up loving these platforms! To be absolutely fair to all the readers, I am definitely using all these companies and they are useful to me! Likely will be useful to you too!

At the same referral and ebook page, you can also download my free ebooks and other free resources.

For quick references to these resources, you can see below.

- Ebooks and other useful resources on enhancing productivity (Investment, Excel, Notion etc). Currently most of it are free at this moment (subject to change).

- WeBull: A powerful brokerage with nice free welcome gift. You can refer to my guide here on how to signup! 4 Simple step only! Click here to register a new account!

- MoneyOwl: You can use this 6SHU-93MC to get free grab vouchers and highly safe liquid cash fund account.

- Trust Bank – You will enjoy free FairPrice E-Voucher referral if you sign up via my referral code KNDBPEPT. Simply download the Trust Bank SG App on the App Store or Google Play Store. Tap on “Use referral code” immediately after you start the app and key in: KNDBPEPT

- FSMOne: P0413007. Good account to keep liquid cash in autosweep and to purchase investment at low fee.

- Hostinger: You can use this link for hosting your new website. 20% off hosting!

- Crypto.com: Use my referral link https://crypto.com/app/h92xdfarkq to sign up for Crypto.com and we both get $25 USD 🙂